Updated:

May 6, 2026

SOC 2 vs SOC 3 – What’s the Difference?

You’ve probably come across SOC reports while researching how to show customers or partners that your company takes security seriously. There are a few types: SOC 1, SOC 2, and SOC 3. It can get a little confusing figuring out which one fits your needs. Most organizations focus on SOC 2, but SOC 3 appears in conversations as well. So how do you know when to choose one over the other?

In this post, we will set SOC 1 aside and focus only on SOC 2 and SOC 3. You will see how they differ, what each one covers, and why your business might choose one depending on your goals and audience.

Key Takeaways

- SOC 2 gives technical, private details for customer reviews; SOC 3 is a short public summary.

- Both use the same audit and follow the same five Trust Services Criteria.

- SOC 2 is for due diligence and vendor reviews; SOC 3 is for marketing and public trust.

- SOC 2 costs more due to control testing; SOC 3 adds minimal cost.

- Only licensed CPA firms can issue these reports, and most companies that get SOC 2 also request SOC 3.

SOC 2 and SOC 3 Definitions

SOC 2 and SOC 3 reports follow standards from the American Institute of Certified Public Accountants (AICPA). Both are used to evaluate how a company protects customer data. If your business stores, processes, or handles client information, especially in SaaS, cloud services, or IT, you will likely need one or both reports, particularly if you’re acting as a service organization for clients managing regulated or financial reporting obligations.

Both reports use the same framework, called the AICPA Trust Services Criteria. These include five categories:

- Security

- Availability

- Processing Integrity

- Confidentiality

- Privacy

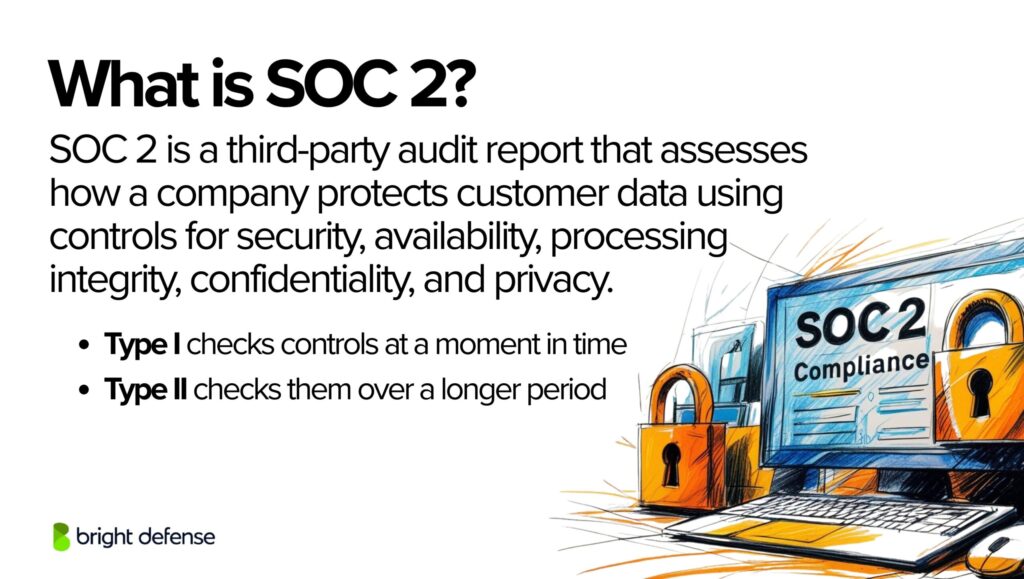

SOC 2 Overview

Every SOC 2 report includes Security. The others are optional depending on what your customers expect or what your services promise. To complete a SOC 2, an independent auditor reviews your systems and policies to check whether your security controls are working as claimed and aligned with your company’s overall security posture.

SOC 2 reports provide detailed information, including technical descriptions, control testing results, and audit findings. Organizations share these reports privately, typically with customers or prospects under NDA, and do not publish them publicly. Teams use SOC 2 as a final report to prove internal controls during compliance or procurement reviews.

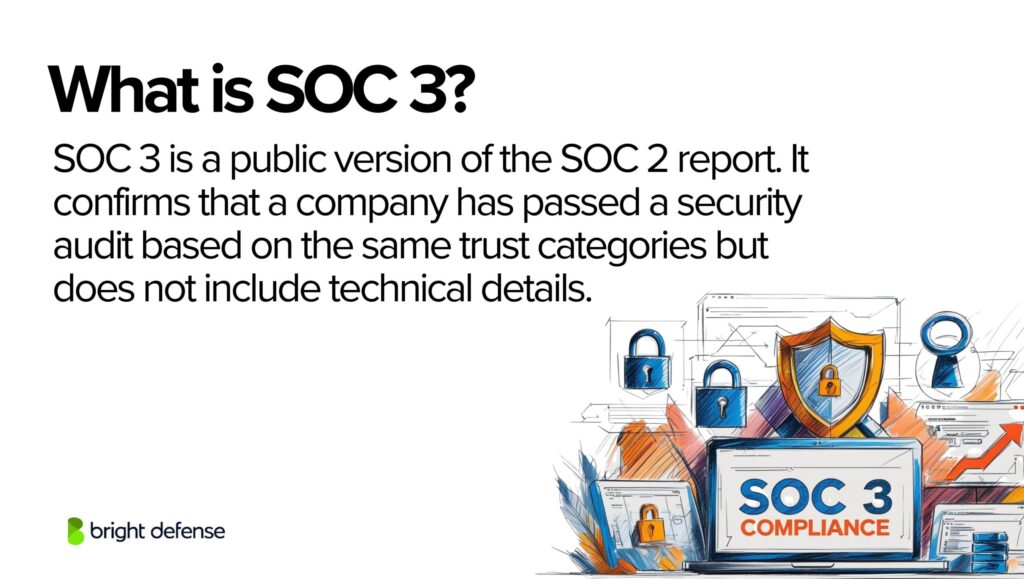

SOC 3 Overview

SOC 3 reports are different. They are based on the same controls as SOC 2 but are much shorter and less technical. You can share a SOC 3 with anyone. Organizations use it publicly and often post it on their websites to show they passed a formal review of their data protection efforts. These reports also serve marketing purposes, helping build trust with a broader audience.

SOC reports are now common across many industries. Many enterprise clients ask for a SOC 2 before moving forward with contracts. AICPA trend data shows consistent growth in SOC 2 audits, especially in cloud and B2B tech sectors.

If your company handles data security responsibilities and works with larger clients, a SOC 2 shows that your internal controls meet industry expectations and support SOC compliance. A SOC 3 gives you a public-facing version to help show credibility without revealing sensitive system details, often reviewed by service organization’s management for external communication.

Similarities and Differences Bteween SOC 2 and SOC 3

Both SOC 2 and SOC 3 reports are based on the AICPA Trust Services Criteria, which include:

- Security

- Availability

- Processing Integrity

- Confidentiality

- Privacy

They use the same audit process. A third-party auditor evaluates whether a company’s systems and controls meet the selected criteria.

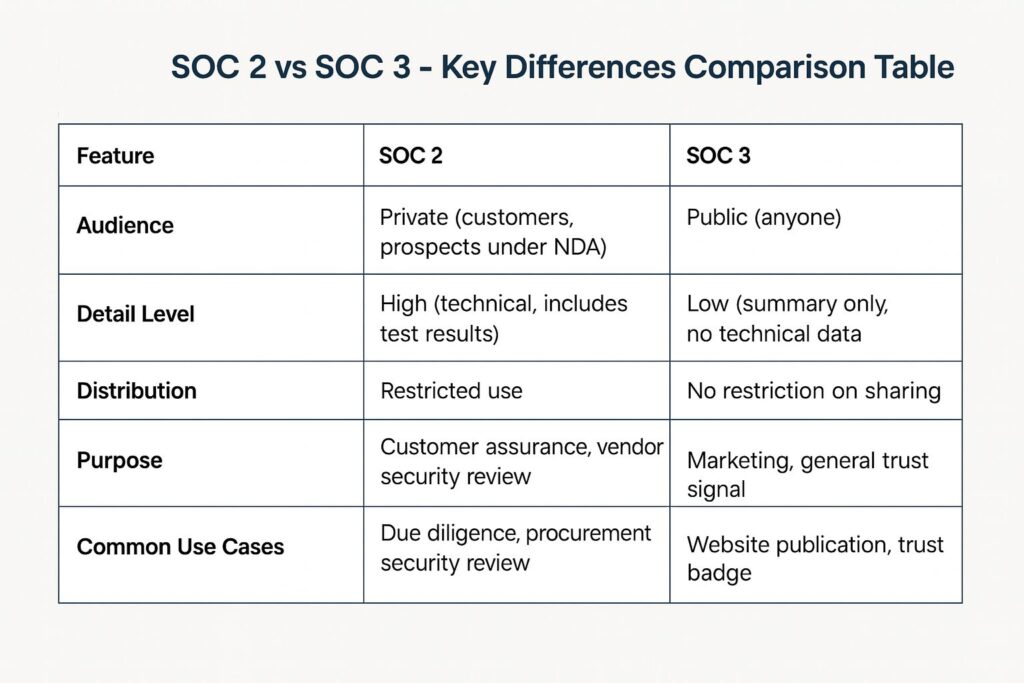

SOC 2 vs SOC 3 – Key Differences Comparison Table

| Aspects | SOC 2 | SOC 2 |

|---|---|---|

| What It Is | Audit report on data security, confidentiality, privacy, processing integrity, availability | Public summary of SOC 2 controls |

| What It Covers | Internal controls that protect customer data | Same SOC 2 controls, but presented in a simplified, non-technical format |

| Who Needs It | Organizations that handle, store, or transmit customer data (e.g., SaaS, cloud providers) | Organizations that want to show proof of security compliance to the general public |

| Who Uses It | Clients, regulators, management (under NDA) | General public |

| Who Requests It | Customers, partners, internal compliance teams | No formal requester — used for marketing or public trust |

| Evaluation Timeline | Type I: At a single point in timeType II: Over a defined period | Always Type II: Based on controls over a defined period |

| When to Get It | When handling customer data and needing to meet vendor or regulatory requirements | When public assurance is needed, without disclosing full control details |

| Reporting | Detailed report (requires NDA) | General-use report (does not require NDA) |

| Reporting |

Practical Example

If a potential customer wants to review your access controls, encryption practices, or how you monitor systems, they will request a SOC 2 report. This report includes those details and shows how they were tested.

If you want to show website visitors or press that your company has passed a third-party audit without disclosing internal systems, you provide a SOC 3. It confirms the result but skips the specifics.

Summary

- SOC 2 is meant for deeper reviews and is shared under strict conditions.

- SOC 3 is meant for public use and acts as a simplified version of the SOC 2.

- Both prove that your controls meet industry standards, but only SOC 2 includes the evidence behind it.

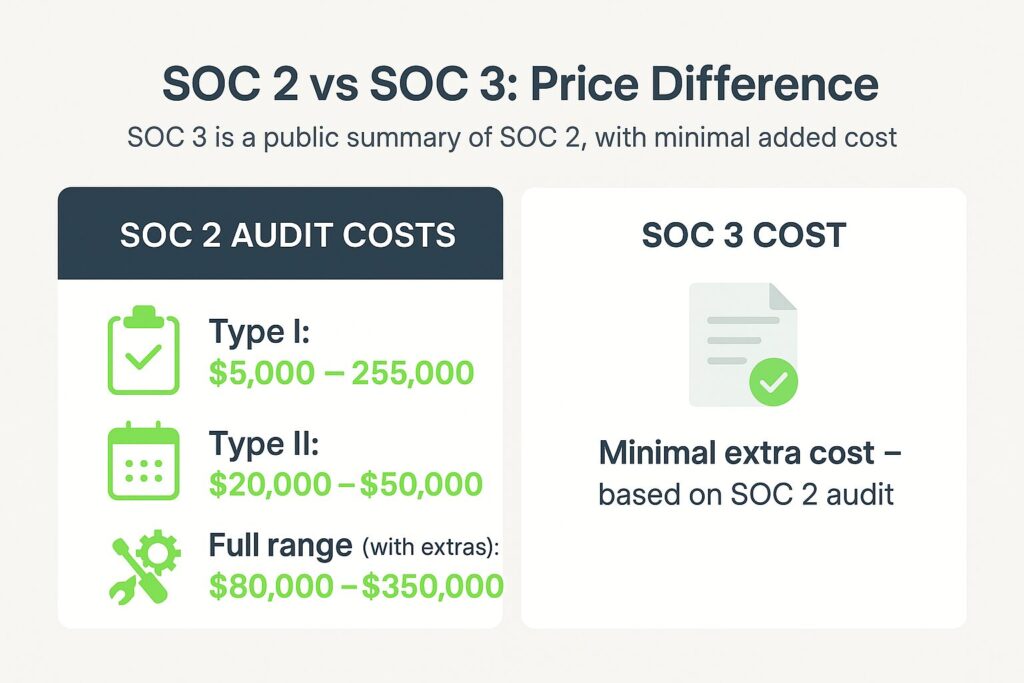

Price Differences Between SOC 2 vs SOC 3

The cost difference between SOC 2 and SOC 3 reports is minimal because both come from the same audit process. SOC 3 is simply a summarized version of SOC 2, meant for public sharing.

SOC 2 Audit Costs

SOC 2 audits are detailed and can be expensive. The price depends on the size and complexity of the company, the number of systems involved, and how many trust categories are included.

- SOC 2 Type I: Evaluates controls at a specific point in time. Costs typically range from $5,000 to $25,000.

- SOC 2 Type II: Assesses the effectiveness of controls over a period (usually 3 to 12 months). Costs often range from $20,000 to $50,000.

Additional costs may include readiness assessments, remediation, and compliance tools. With all factors included, total expenses can range between $80,000 and $350,000.

SOC 3 Report Costs

A SOC 3 report uses the results of the SOC 2 audit. It does not require a separate audit or testing process. Because of this, the extra cost to produce a SOC 3 is usually small. Some audit firms include it as part of the SOC 2 package, or charge a minor fee for formatting and issuing the public version.

Summary

- SOC 2 is the primary cost driver due to its depth and control testing.

- SOC 3 adds little or no extra cost, since it’s derived from the same audit.

- Most companies that produce SOC 2 reports also request a SOC 3 to serve public audiences without disclosing sensitive information.

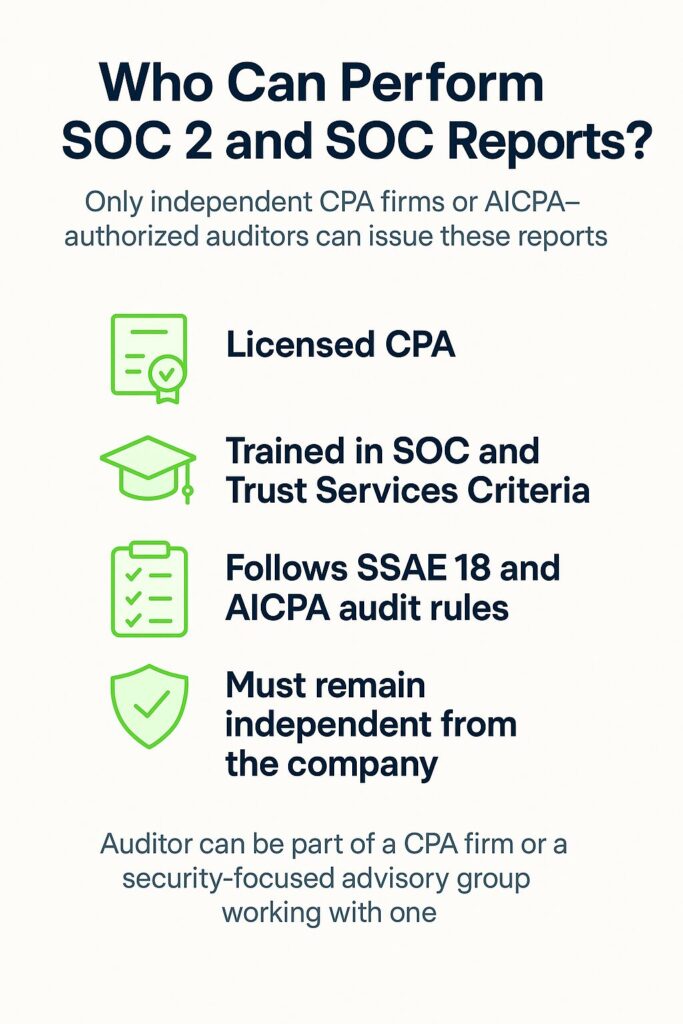

Who Can Perform SOC 2 and SOC 3 Reports?

Only independent CPA (Certified Public Accountant) firms or firms authorized by the American Institute of Certified Public Accountants (AICPA) can conduct SOC 2 and SOC 3 audits and issue the official reports.

These firms must follow the AICPA’s Statement on Standards for Attestation Engagements (SSAE 18) guidelines and assess compliance with the AICPA’s Trust Services Criteria.

To issue either a SOC 2 or SOC 3 report, the auditor must:

- Hold an active CPA license

- Be trained in SOC reporting standards and Trust Services Criteria

- Follow AICPA audit methodology and quality control requirements

- Maintain independence from the company being audited

The auditor can work directly for a CPA firm or be part of a cybersecurity-focused advisory group partnered with a licensed CPA firm. These evaluations result in restricted use reports for SOC 2 or general use reports for SOC 3, depending on the report type and distribution intent.

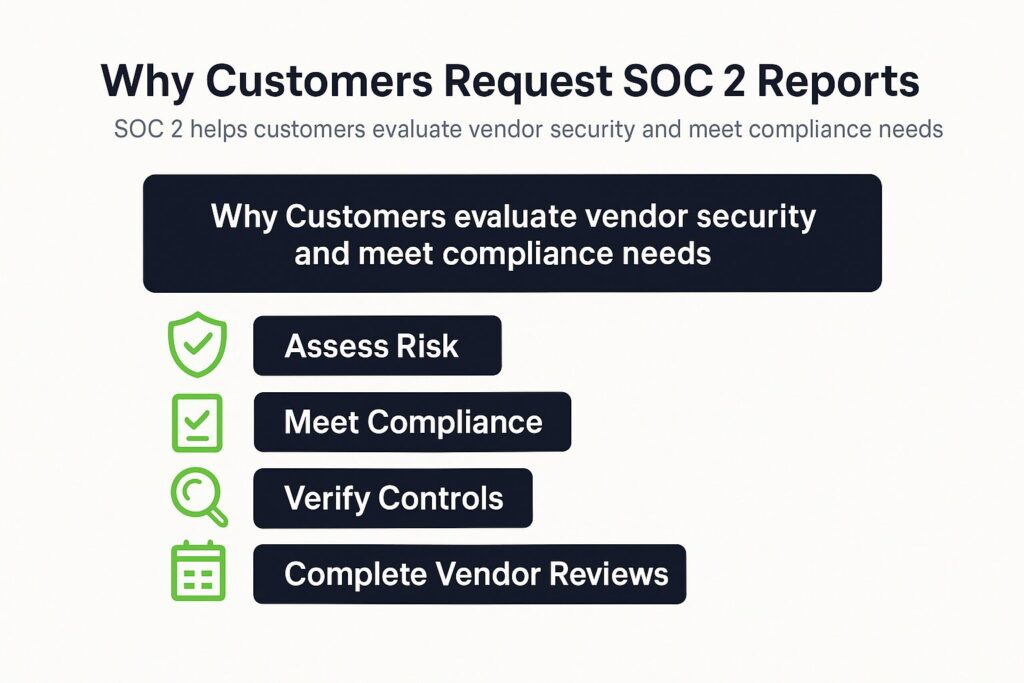

Why Customers Request SOC 2 Reports

SOC 2 reports are designed for customers who need detailed insight into how your company secures its systems and handles data. They request these reports to:

- Evaluate Risk: Security, availability, and confidentiality controls directly affect business risk. A SOC 2 report helps customers decide if your systems are safe to use and supports confidence in your information security practices.

- Meet Internal Compliance: Many organizations have internal or regulatory requirements (such as HIPAA, PCI, or GDPR) that demand proof of vendor controls, especially when handling financial information or regulated workloads.

- Review Specific Controls: SOC 2 includes detailed testing results, control descriptions, and evidence of how your company operates over time. Customers may want to verify practices like access control, encryption, and incident response, especially if you’re dealing with sensitive data.

- Satisfy Procurement Checklists: For enterprise buyers, SOC 2 is often a box to check during security due diligence before contracts are signed. A readiness assessment can also help prepare for these evaluations.

- Avoid Additional Audits: A strong SOC 2 can reduce the need for separate security questionnaires or site visits, saving time for both sides and demonstrating your organization’s ability to maintain strong controls.

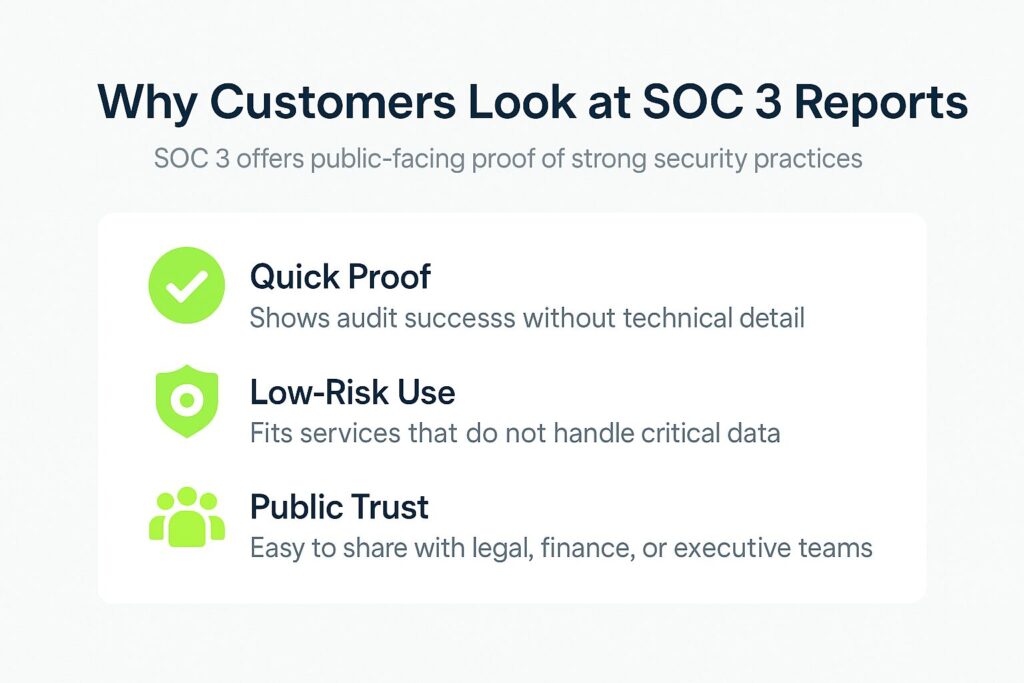

Why Customers Request SOC 3 Reports?

SOC 3 reports are requested less often, but they still provide value in certain cases:

- Quick Assurance: A customer may want fast proof that your company passed a SOC audit without reviewing technical details.

- Low-Risk Partnerships: When the service does not involve critical data or infrastructure, a SOC 3 may be enough. These cases often apply to companies that offer services not tied to regulated systems.

- Public Credibility: Non-technical stakeholders such as legal, finance, or executive teams can review SOC 3 reports to assess a company’s trustworthiness. Companies that focus on transparency in their marketing use SOC 3 as a helpful trust signal.

SOC 2 vs SOC 3: Final Take

SOC 2 and SOC 3 reports serve different purposes. SOC 2 provides detailed, private insights into your security controls. SOC 3 offers a high-level summary you can share publicly. Both help build trust, but they’re used in different ways depending on the audience.

Bright Defense helps you decide which report fits your needs and guides you through the audit process. We connect to your systems, monitor for risks, and help you stay prepared with less manual work. Our process supports both service providers handling sensitive information and organizations preparing reports for the general public.

Ready to get started? Reach out to Bright Defense to begin your compliance automation and SOC reporting.

FAQs

A SOC 2 report is designed for users who need detailed information and assurance about controls at a service organization that relate to the Trust Services Criteria categories in scope

A SOC 3 report addresses controls relevant to the same Trust Services Criteria areas as SOC 2 but presents less detail, which is why it is treated as a general use report

Yes, SOC 3 can be freely distributed, while SOC 2 is commonly treated as restricted use in many vendor programs

Yes, SOC 2 provides more detail, while SOC 3 does not provide the same level of detail

Yes, both relate to Security and can include Availability, Processing Integrity, Confidentiality, and Privacy depending on scope

Yes, SOC 3 is structured for broad distribution, and AWS describes its SOC 3 as a publicly available summary of its SOC 2 report

Yes, SOC 2 is intended for readers who need detailed assurance information, while SOC 3 is the lighter public-facing option

A SOC 2 report is the usual next request when you need deeper detail than SOC 3 provides, and many vendors distribute SOC 2 under NDA while keeping SOC 3 public search

SOC 2 reports provide detailed control information and testing results for specific users, while SOC 3 reports cover the same Trust Services Criteria topics at a higher level with far less detail for broader sharing.

SOC 3 is not restricted because AICPA treats it as a general-use report that can be freely distributed.

L1 analysts monitor tools and perform initial alert triage and escalation, L2 analysts investigate higher-priority incidents and drive containment and recovery actions, and L3 analysts handle major escalations plus threat hunting and advanced testing oversight.

Get In Touch

-min")